A review of Altaroc’s “Basic Building Block”

Summary

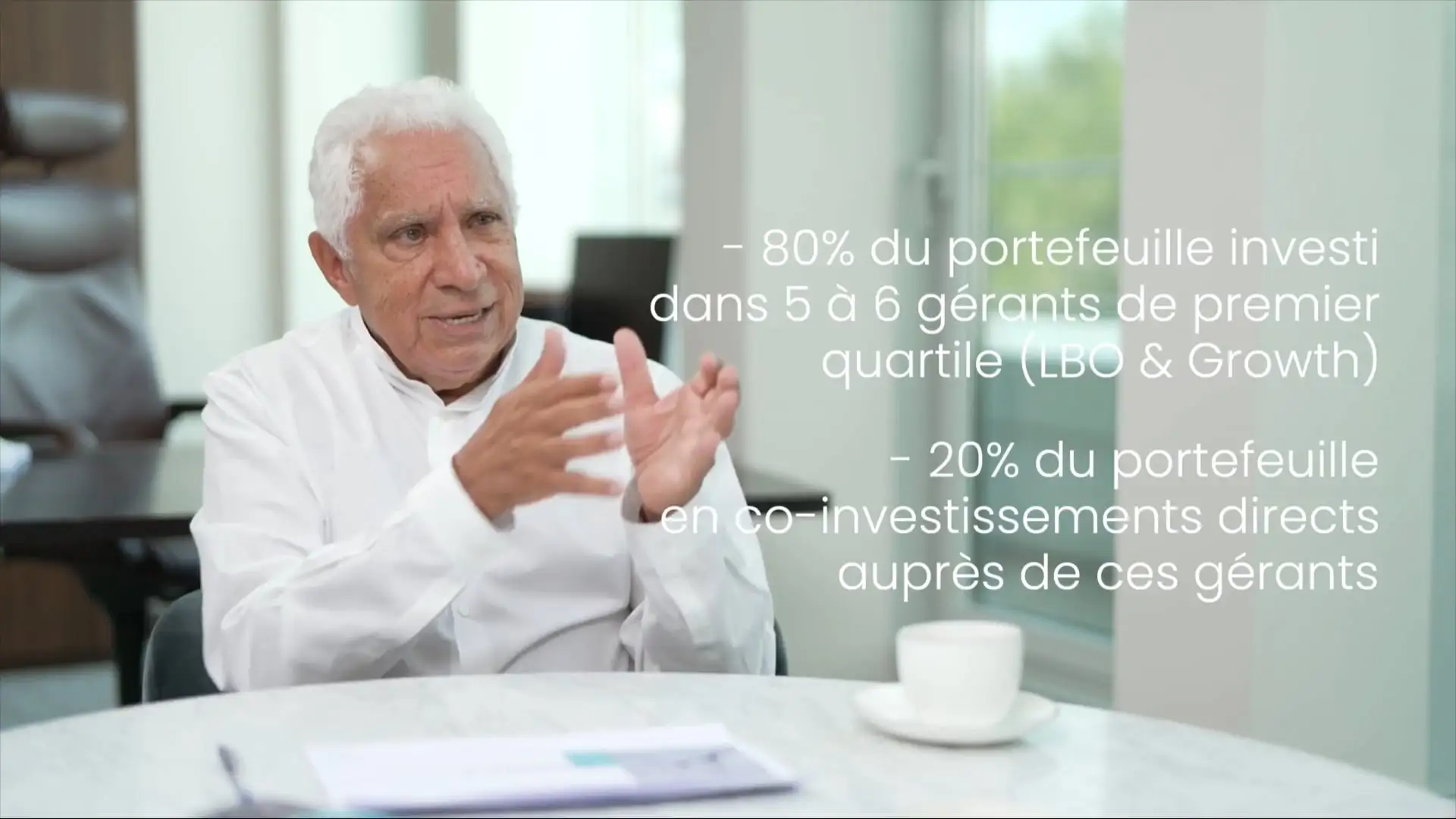

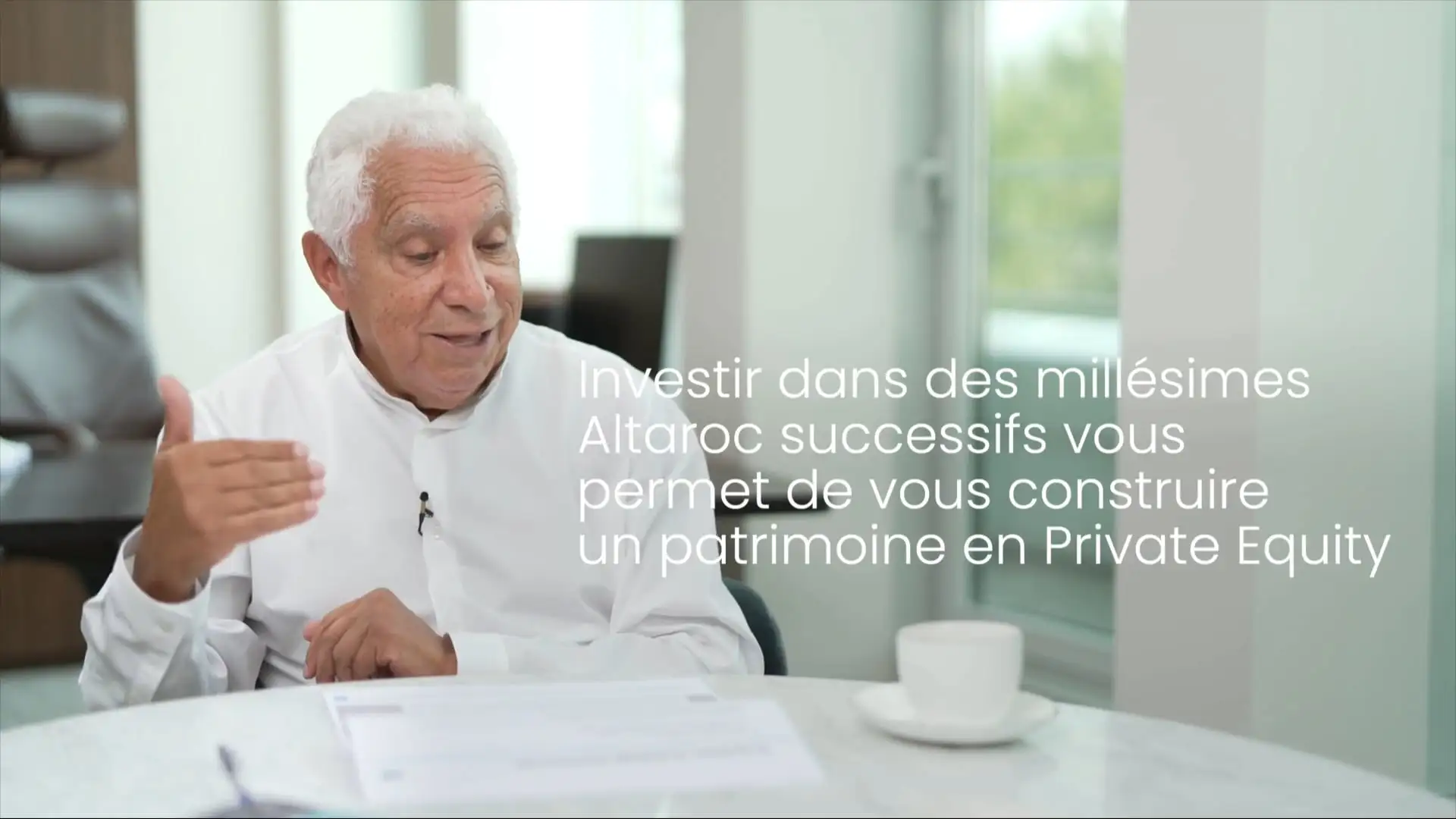

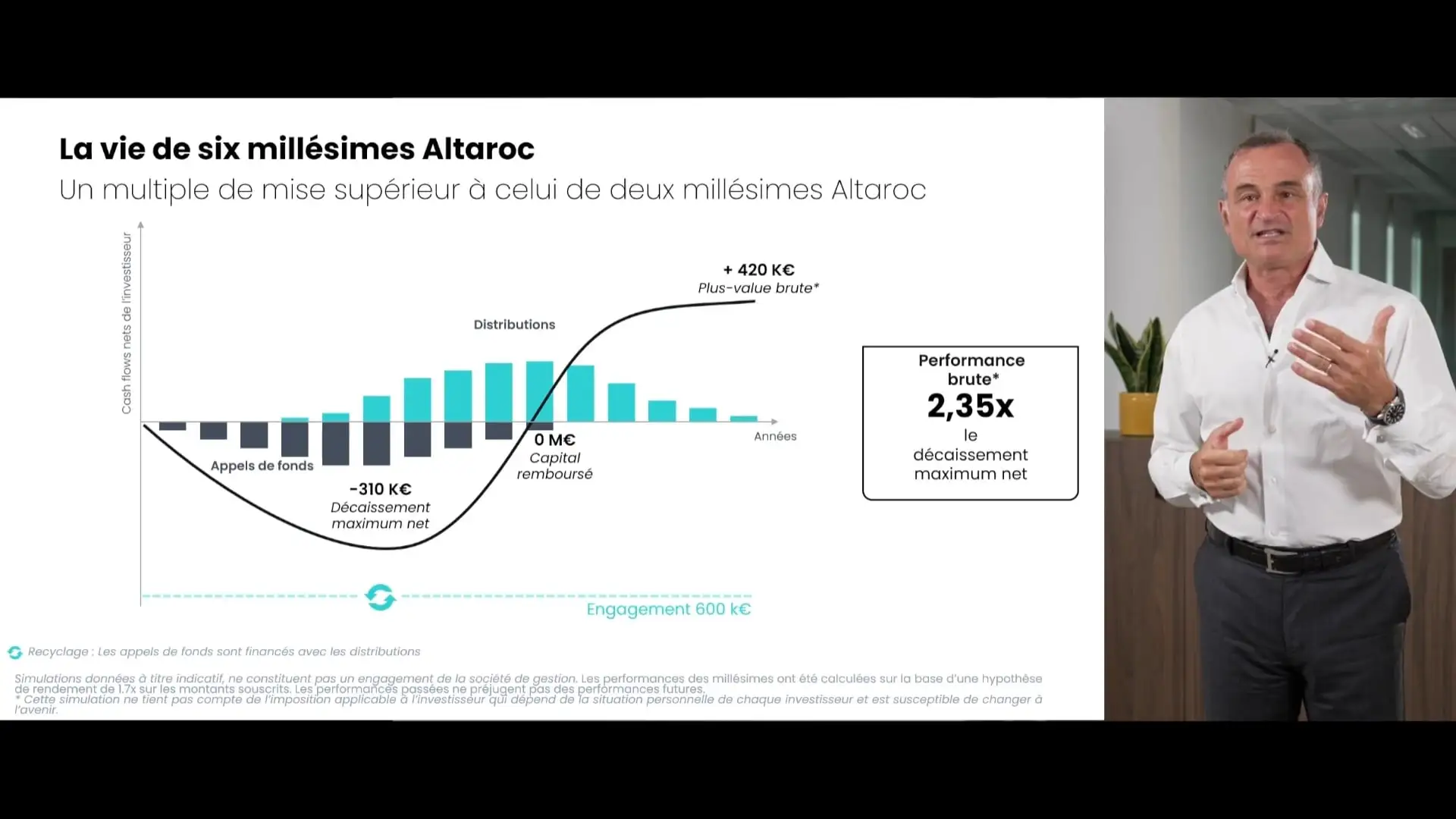

Frédéric Stolar explains the fundamental structure of an Altaroc vintage, the cornerstone of the firm’s offering. Each vintage provides access to a structured portfolio comprising 80% of top-tier global private equity funds and 20% of co-investments made alongside these managers, with no fees or carried interest. This structure allows investors to access exceptional investment opportunities while optimizing costs. One ofAltaroc key differentiatorsAltaroc the predictability of its cash flows. Unlike traditional funds where capital calls are uncertain, Altaroc a clear subscription structure with scheduled calls of 20% per year over five years. This visibility enables simplified and proactive cash flow management. Cash flow operations also rely on a recycling mechanism. Starting in the fourth year, the first distributions partially finance subsequent capital calls. Thus, for a commitment of €100,000, the capital actually invested (drawn down) is reduced to approximately €80,000. This approach improves the efficiency of invested capital, as the investor commits less cash while maintaining the same potential for returns. In terms of returns, the model remains essentially unchanged. The investor recovers their capital around the seventh year and then receives the gains in subsequent years. Performance can thus be expressed in two ways: approximately 1.7x on committed capital or nearly 1.9x on actual invested capital. This dual perspective highlights the power of capital recycling andAltaroc abilityAltaroc optimize the return on capital at work.Ultimately, the Altarocstands out for its combination of diversification, cash flow visibility, investment discipline, and performance optimization, making private equity more transparent and accessible to private investors.